Anybody else remember the drop of your stomach when your folks drove a hilly country road and you weren’t expecting the quick downhill drop? We never knew when the highs and lows or the next turn was coming—sounds a lot like the markets, doesn’t it?

Where are you on the ride? Check out Caitie’s take on thrill rides and the rhythms of the markets this week

Want content like this in your inbox each week? Leave your email here.

As we know, the markets go up and down. It’s just part of the deal! But sometimes the peaks and drops can get a little intense, so it’s worth revisiting this reality once in a while.

The most mindful long-term investors are usually less alarmed by the bumps along the way. They know what they’ve got is basically a lifetime pass on a rollercoaster. But it’s the ride to greater potential returns, so they can keep the thrills in perspective.

What would the alternative be, in our rollercoaster example? If you get spooked on a big drop, there’s no abandoning your seat. “Please keep your hands, arms, feet, and legs inside the vehicle while on this ride,” the announcement cautions.

It’s best to stay in your seat, your best chance to get to the end of the ride in one piece.

As long-term investors, we know that we can afford to let each cycle just run its course. Jumping off the ride partway through sets us up for more trouble and more work than it would ever be worth: how would we know when it’s best to jump back on? How do we know that we’ll be able to jump safely?

We hope this is context enough to allow us to be blunt with you: long-term investing is a ticket for the whole ride, whatever that may mean.

Selling out? Selling out is a one-way ticket out of our shop.

Your resources are your business. Where you park your wealth is your decision, completely, and each one of us needs to do what is best for them.

But we choose to keep at it for those who are thinking about the long haul. We believe it’s the most effective approach to a lifetime of financial wellbeing—and whatever legacy might stretch beyond your lifetime!

Clients, we strive to communicate our values and intentions clearly. Do you need to clarify anything with us? Call or write, anytime.

Want content like this in your inbox each week? Leave your email here.

We’ve talked before about how the ups and downs of the market are like being on a rollercoaster. The anticipation, the buildup—those things don’t have to be scary when we understand they’re part of the ride. For some, they’re even thrilling.

This comparison is a little simplistic, sure. But there are valuable lessons in this image.

For instance, one difference between the markets and actual rollercoasters is that the peaks and valleys of the stock charts aren’t being designed by skilled engineers. Charts are historical: their goal is to map the ride that happened, not the best possible ride.

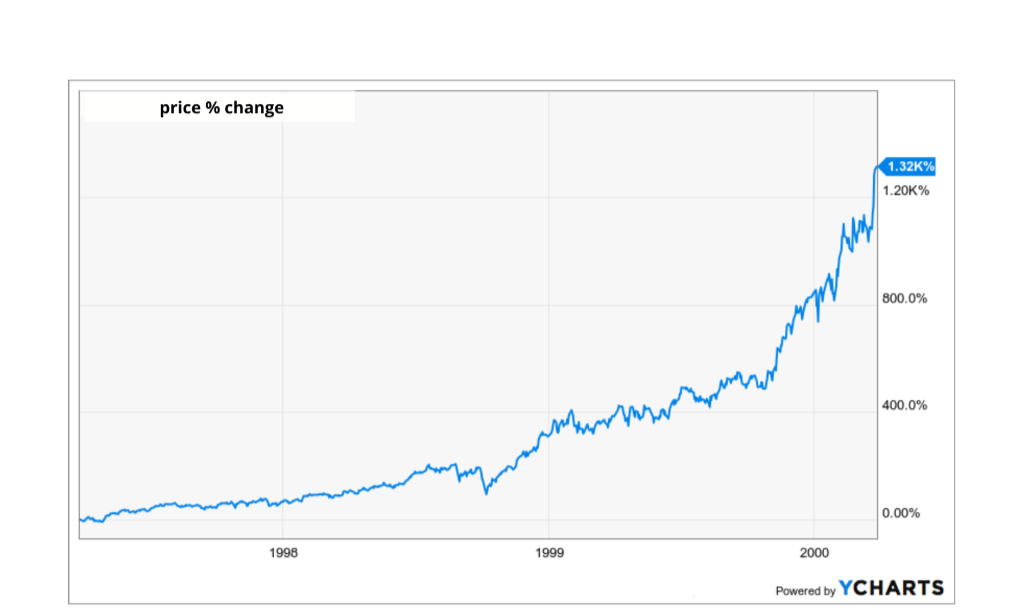

Take this example: as shown in the chart below, this company’s stock price climbed quickly during the tech boom. You can almost hear the coaster gaining steam—nearly vertical.

The company’s pre-2000 ascent.

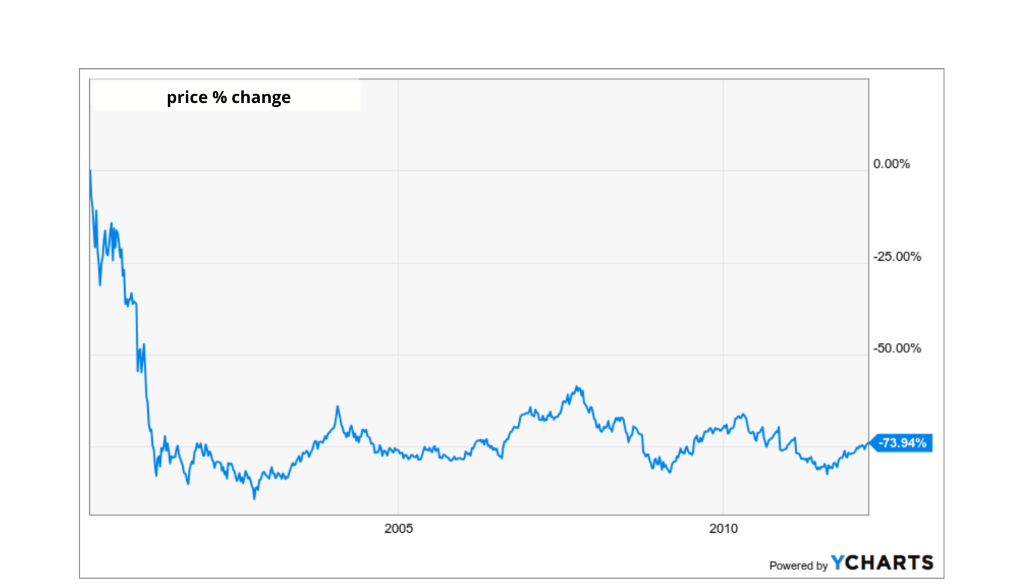

And then, as with all thrill rides, the drop (pictured below). Some investors aren’t sure which fell faster: the price or their stomachs. A rollercoaster engineer would be able to design that part in a way that riders would forgive them the jarring rise and fall.

But what came next would probably get a rollercoaster engineer fired.

The company’s post-2000 fall.

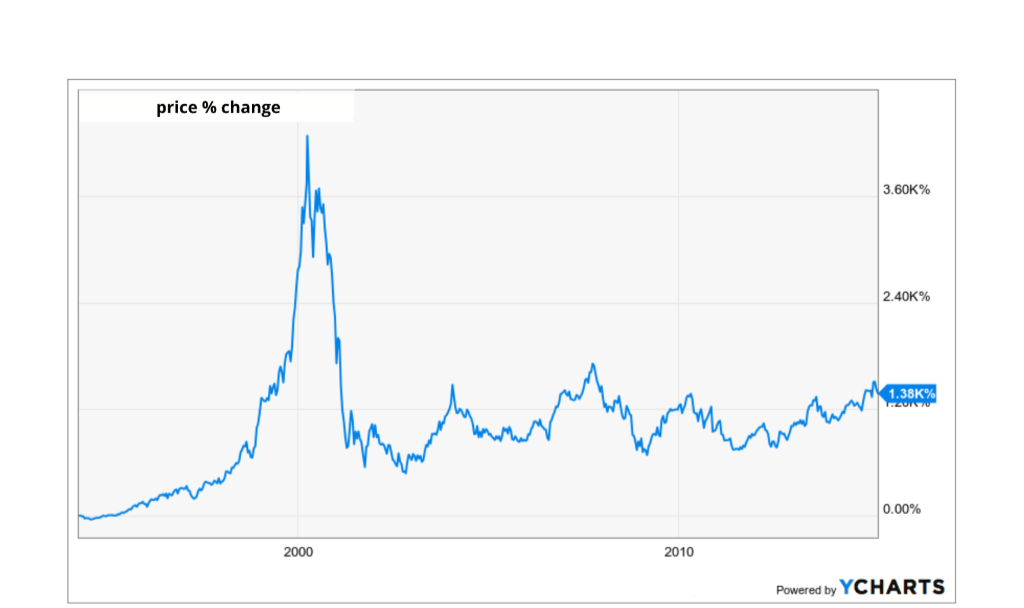

After the pop in 2000, the stock price balanced out. No more steep climbs: the thrill ride became a lazy river through the lowlands. Investors who held for the climb, and the subsequent drop, expected another climb. But the thrill was gone; the ride wasn’t the same.

The map of the company’s whole ride.

Okay, we’ll drop the coaster-cum-lazy-river comparison. You may have realized by this point that what we’ve just described is a historical example of a bubble: an excess of hype that ends with a pop!

We mentioned that charts are maps of where things have been, so the lesson isn’t necessarily that they tell us where that specific thing is headed next… but they may be instructive in spotting similar rides in the future.

Is it a thrill we’re game for? Or is it shaping up to be a thrill we’re not interested in, like the pop of a bubble?

Clients, let us know when you have questions or want to hear more about what this all means for you.

Want content like this in your inbox each week? Leave your email here.

With summer fading in such a strange year, we find ourselves revisiting old memories. This will date me, but I’m thinking about the summer thrills we used to enjoy at places like Omaha’s Peony Park or Lake Okoboji’s Arnolds Park.

Part of the fun of a thrill ride is the anticipation. There’s a story and a rhythm to each ride. On a coaster, you make the climb—with a thunk-thunk-thunk on a lot of those “classic” rides!—and you can see the drop coming. Although you won’t know what they feel like until you get there, you can see the curves ahead.

And it’s all fleeting. The climb may feel like it takes forever, the terror of the drop may flash your life before your eyes… but you don’t go up and up forever, and you don’t fall down and down forever.

Sound familiar? Clients, you’ve heard us say this exact thing as a reminder about the markets.

Part of this lesson could use more attention, though: the ride can just be a ride when we know where we are on it.

When investors enjoy the climb of a hot stock, some mistakenly rush to throw everything they have at it, not recognizing that they are already near the peak: that thing will not go up and up forever. Nothing does. (Incidentally, this exuberant behavior can contribute to bubbles.)

Likewise, some get the itch to sell out when a stock cools off—but things may just be down for now and not down forever.

We don’t have a crystal ball, and we don’t have a map, but we know there are rhythms and cycles. What pain could we save ourselves by using a little perspective?

Where are we on the ride?

Clients, we’re here to help make sense of your plans and planning. Call or email when you’re ready for us.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual.

As long term investors we talk a lot about the need to weather short-term volatility in pursuit of long-term results. Our notion is that volatility is not risk, but an inherent feature of investing.

As years go by, many think of the market as having good years and bad years. This is based on the outcome for calendar years. The astonishing thing is how much movement there is during the course of the typical year.

“At least one year in four, roughly, the market declines.” We’ve said that about a billion times, to reiterate that our accounts are likely to also have good years and bad years, if one judges on annual returns. The object is to make a decent return over the whole course of the economic cycle, year by year and decade by decade.

But in those other three years out of four, the market also experiences declines during the course of the year. In an average year you may see a decline of 10 to 15% at some point during the year.

Our object is to leave long term money to work through the ups and downs, without selling out at a bad time. Three things help us do that:

1. A sense that everything will work out eventually, a mindset of optimism.

2. Awareness that downturns tend to be temporary, ultimately yielding to long term growth in the economy.

3. Knowing where our needed cash will come from, based on a sound cash flow plan.

Bottom line, even years that end up well can give us a rough ride. Knowing this can make it easier to deal with.

Clients, if you would like to talk about this or anything else, please email us or call.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Stock investing involves risk including loss of principal.

All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

You must be logged in to post a comment.