We’ve talked before about how the ups and downs of the market are like being on a rollercoaster. The anticipation, the buildup—those things don’t have to be scary when we understand they’re part of the ride. For some, they’re even thrilling.

This comparison is a little simplistic, sure. But there are valuable lessons in this image.

For instance, one difference between the markets and actual rollercoasters is that the peaks and valleys of the stock charts aren’t being designed by skilled engineers. Charts are historical: their goal is to map the ride that happened, not the best possible ride.

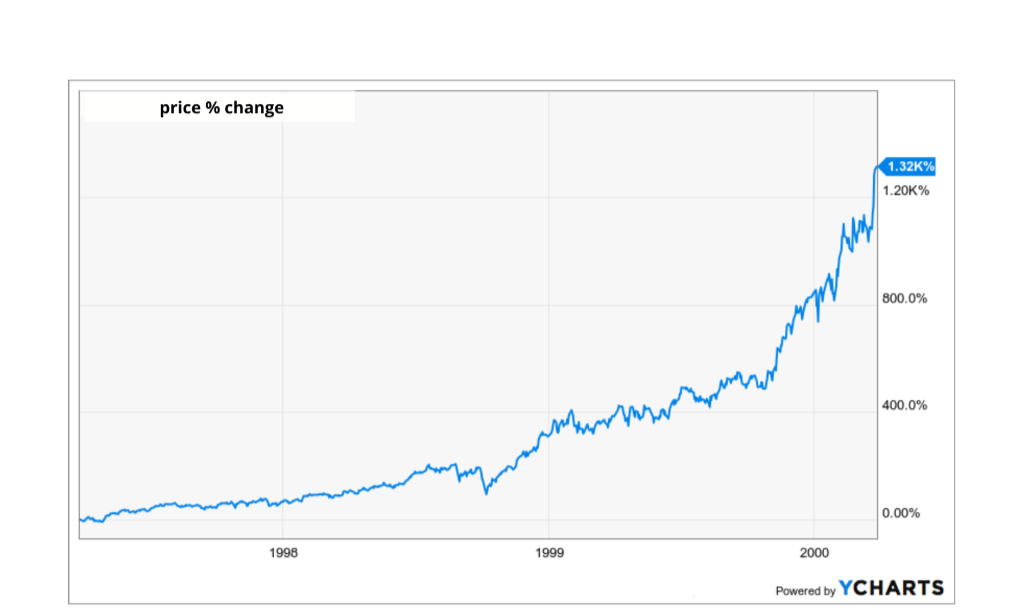

Take this example: as shown in the chart below, this company’s stock price climbed quickly during the tech boom. You can almost hear the coaster gaining steam—nearly vertical.

The company’s pre-2000 ascent.

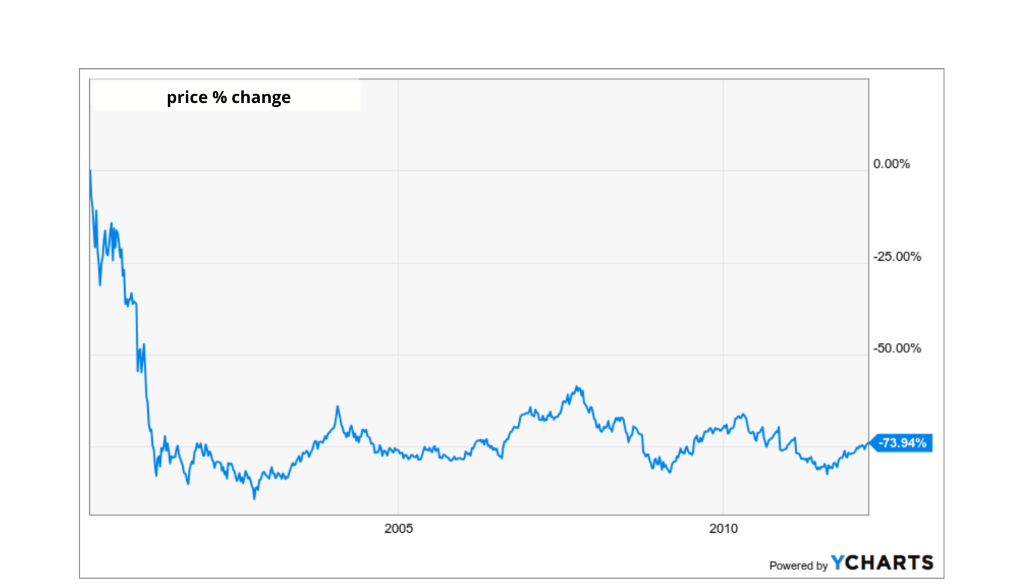

And then, as with all thrill rides, the drop (pictured below). Some investors aren’t sure which fell faster: the price or their stomachs. A rollercoaster engineer would be able to design that part in a way that riders would forgive them the jarring rise and fall.

But what came next would probably get a rollercoaster engineer fired.

The company’s post-2000 fall.

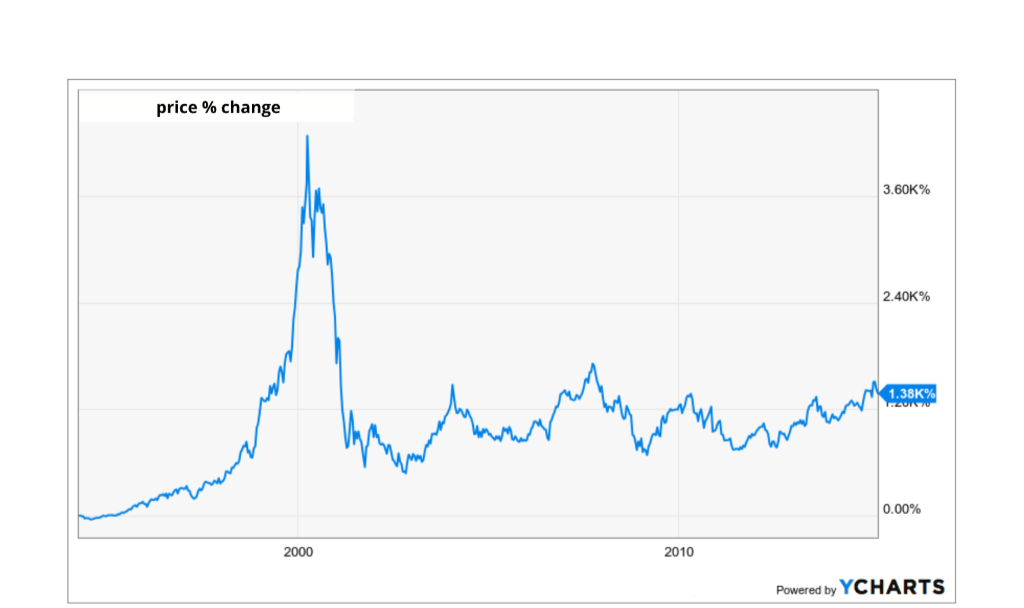

After the pop in 2000, the stock price balanced out. No more steep climbs: the thrill ride became a lazy river through the lowlands. Investors who held for the climb, and the subsequent drop, expected another climb. But the thrill was gone; the ride wasn’t the same.

The map of the company’s whole ride.

Okay, we’ll drop the coaster-cum-lazy-river comparison. You may have realized by this point that what we’ve just described is a historical example of a bubble: an excess of hype that ends with a pop!

We mentioned that charts are maps of where things have been, so the lesson isn’t necessarily that they tell us where that specific thing is headed next… but they may be instructive in spotting similar rides in the future.

Is it a thrill we’re game for? Or is it shaping up to be a thrill we’re not interested in, like the pop of a bubble?

Clients, let us know when you have questions or want to hear more about what this all means for you.

Want content like this in your inbox each week? Leave your email here.

You must be logged in to post a comment.